Key Takeaways

Policy Statement 1: Empowering the Registrar to Determine Sustainability Reporting Requirements

Currently, there are no specific provisions under Subdivision 1, Division 3, Part III of the Act relating to sustainability and non-financial information reporting. The disclosures of sustainability-related information in the directors’ report are optional as prescribed in section 253(3) of the Act. Therefore, omission of the matters prescribed in section 253(3) would not result in non-compliance.

SSM proposes empowering the Registrar to prescribe sustainability reporting requirements for qualifying NLCos using a mandatory “comply or explain” approach. Under this framework, companies that are unable to fully comply with disclosure requirements must provide clear and reasoned explanations for non-compliance, including details of data gaps, operational limitations or transition challenges.

The proposed changes will primarily affect Subdivision 1, Division 3, Part III of the Act relating to financial statements and reports.

By comparison, sustainability and non-financial information disclosures are mandatory for companies subject to sections 414CA(A1) and 414CB(A1) of the UK’s Companies Act 2006 and form part of the strategic report prepared by directors. In Australia, sustainability disclosures are mandatory and embedded into primary legislation under section 292A of the Corporations Act 2001. In Singapore, sustainability reporting was initially introduced under a “comply or explain” approach and subsequently became mandatory under SGX Listing Rule 711A and the ACRA Climate Reporting Roadmap.

Malaysia’s approach of starting with “comply or explain” therefore mirrors Singapore’s earlier trajectory and is a pragmatic recognition of the NLCo ecosystem’s current readiness.

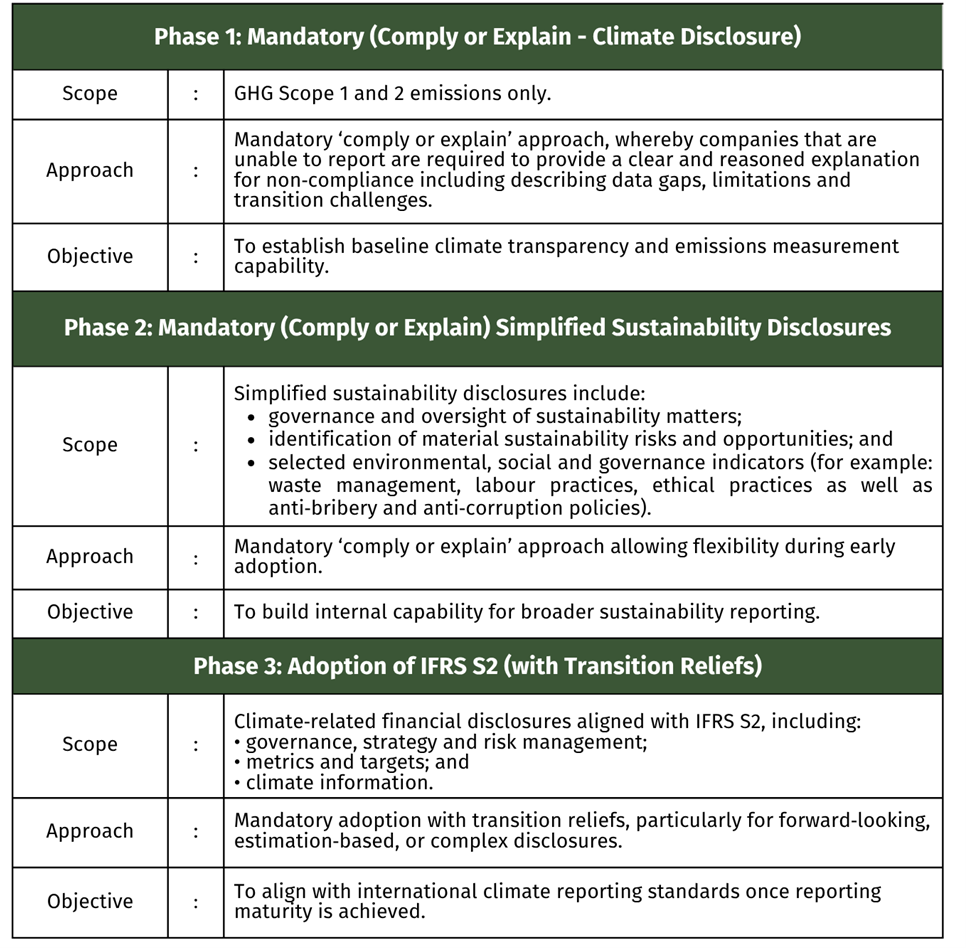

Policy Statement 2: Introduction of a Phased Sustainability Reporting Framework

The comparative analysis across jurisdictions demonstrates a trend towards a climate-first approach, whereby jurisdictions prioritise climate-related disclosures, particularly Scope 1 and 2 GHG emissions, before expanding to broader sustainability topics and more complex reporting requirements.

SSM adopts this same “climate-first” sequencing:

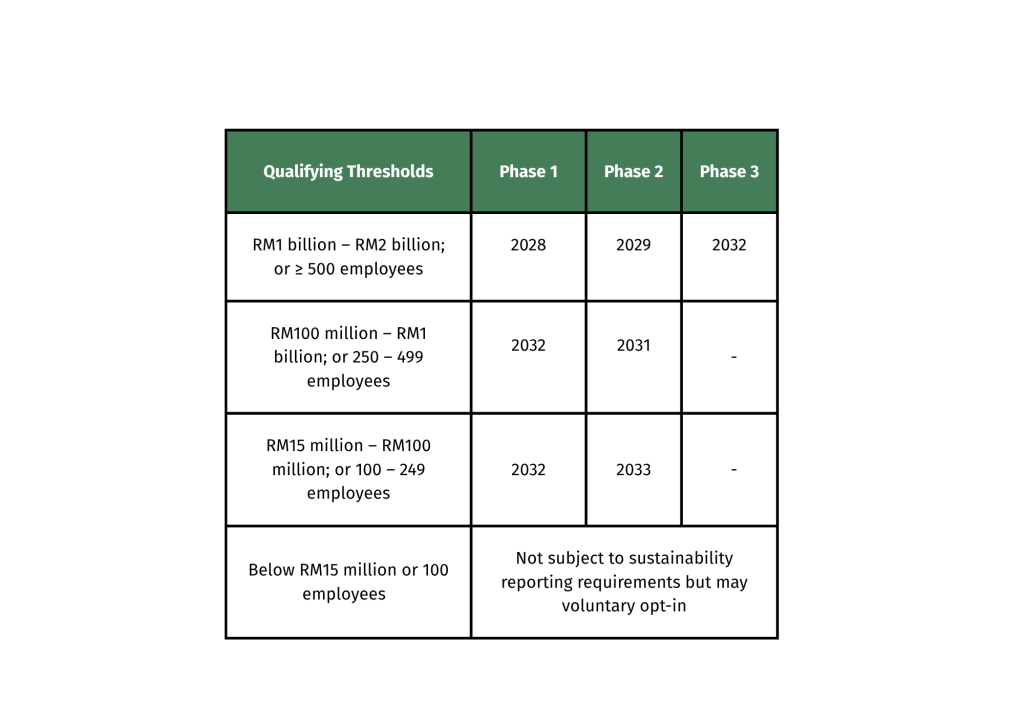

(i) Thresholds and Proposed Implementation Timelines

Recognising that NLCOs vary significantly in size and reporting readiness, SSM proposes a phased threshold-based approach based on annual revenue and employee count:

Notably, smaller companies below the threshold may voluntarily opt into the framework but would be required to fully comply if they do so. This means that a smaller company choosing to opt in for commercial or reputational reasons, for instance to satisfy supply chain ESG requirements, loses the benefit of the “comply or explain” flexibility enjoyed by companies that are mandatorily captured. Businesses below the threshold should weigh this carefully before voluntarily opting in.

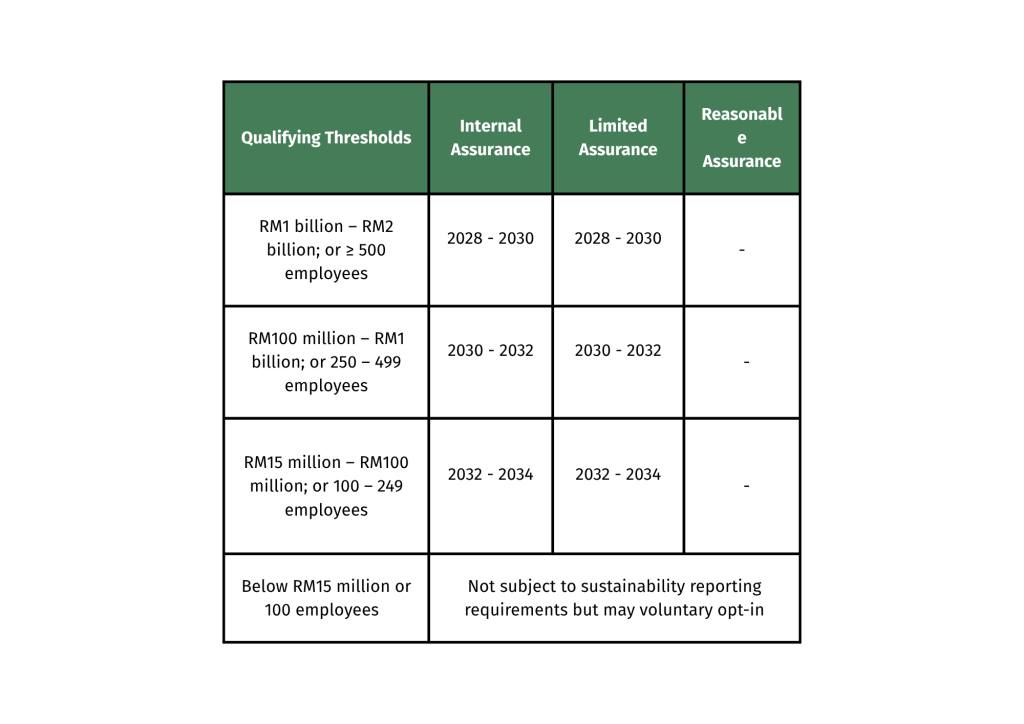

(ii) Assurance Framework

SSM also proposes introducing a phased assurance framework for sustainability disclosures. The proposed model mirrors approaches adopted in other jurisdictions where limited assurance is introduced before moving towards more rigorous assurance requirements.

Policy Statement 3: Strengthening directors’ accountability for sustainability and non-financial information disclosures

At present, sustainability-related information in directors’ reports remains optional under section 253(3) of the Act. As a result, omission of such disclosures does not currently trigger statutory non-compliance penalties.

SSM now proposes to make sustainability and non-financial disclosures part of directors’ mandatory statutory reporting responsibilities.

This means directors may face legal exposure for non-compliance in a manner similar to existing obligations relating to financial reporting under section 252(5) of the Act. The proposal signals a clear regulatory shift: ESG disclosure is no longer viewed merely as a reputational or investor-relations exercise, but increasingly as a governance and compliance obligation.

Policy Statement 4: Enhancing the Act to incorporate Sustainability Assurance Provider framework

To support the proposed assurance requirements, SSM also proposes establishing a statutory framework for Sustainability Assurance Providers (“SAPs”). Instead of creating an entirely separate regime, SSM proposes expanding the definition of “auditor” under the Companies Act 2016 to include SAPs for sustainability assurance purposes.

Proposed Minimum Qualifications for SAPs

SSM proposes that SAPs should:

(a) possess a degree or diploma from educational institutions recognised by the Malaysian Qualifications Agency or any other relevant professional qualifications;

(b) have at least five years’ experience in conducting audit or assurance engagements; and

(c) obtain approval as a sustainability assurance provider from the Minister.

The proposal reflects growing regulatory recognition that ESG reporting will require credible verification mechanisms and specialised assurance expertise.

Why This Matters for Your Businesses

The proposed amendments represent one of Malaysia’s most significant ESG regulatory developments to date for non-listed companies.

While implementation will occur progressively, the direction of travel is increasingly clear:

Public Consultation

The SSM invites comments to the Consultative Document until 2 June 2026. Businesses are encouraged to engage substantively with these questions, as the responses will directly inform the shape of the final amendments.

The consultation questions can be accessed here.

If you have any query, please contact the author, Joyce Ong Kar Yee, Partner in the ESG and Sustainability Practice (oky@lh-ag.com). This article was co-authored by Hannah Jasmin binti Jefferelli, Pupil.