On 20 September 2024, Malaysia launched the Single Family Office (“SFO”) Incentive Scheme as part of its broader strategy to transform Forest City as a premier Special Financial Zone (“SFZ”). Designed to attract ultra-high-net-worth (“UNHW”) families, the scheme offers significant tax incentives, regulatory support, and operational flexibility to encourage the establishment of family offices in Malaysia.

Shortly after the launch, the Securities Commission Malaysia (“SC”) issued a comprehensive FAQ outlining the eligibility criteria, application process, and benefits available under the scheme. To promote awareness, the SC also hosted the Single Family Office Summit, where regulators highlighted the strategic role of SFOs in mobilising family capital for long-term growth.

This alert summarises the key requirements, incentives, and compliance steps for setting up a SFO in Forest City SFZ.

What is an SFO?

A SFO is a privately controlled corporate vehicle established by members of a single wealthy family to manage the family’s investments, assets, and long-term interests.

Key Components of an SFO Structure

Prospective families must establish the following two entities, which form the core operating and investment structure of the SFO in Malaysia.

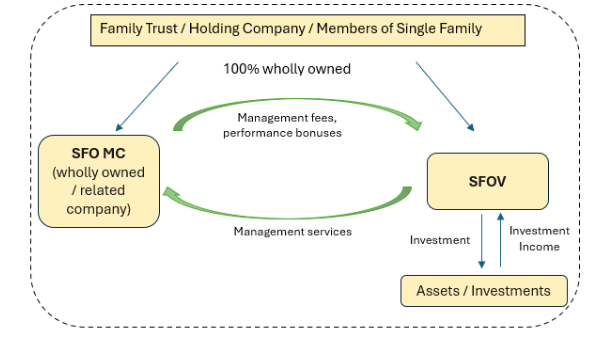

1. Single Family Office Vehicle (“SFOV”)

a. A corporate entity wholly owned or controlled by members of a single wealthy family.

b. Its sole purpose is to hold and manage the family’s assets, investments, and long-term interests.

c. Acts as the family’s principal investment holding company under the scheme.

2. Single Family Office Management Company (“SFO MC”)

a. An entity that provides exclusive management services to its related SFOV.

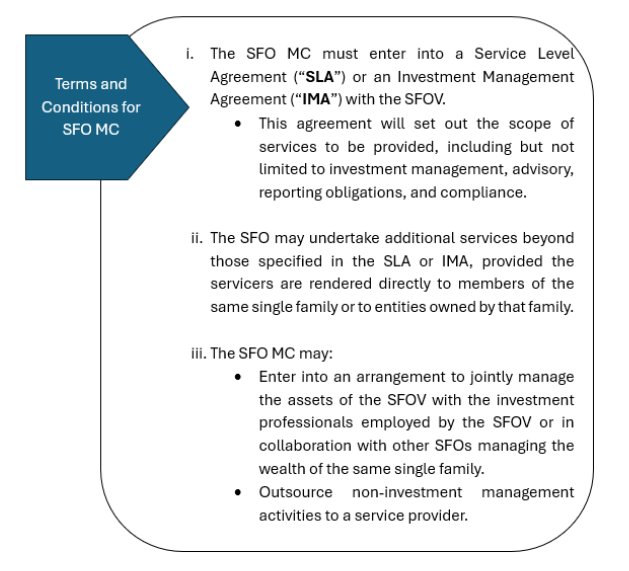

b. Responsible for a wide range of functions, including:

Tax Incentives, Licensing & Requirements[1]

1. Initial 10-year Period (“Initial Period”)

|

Criteria |

SFOV |

SFO MC |

|

Tax Incentive[2] |

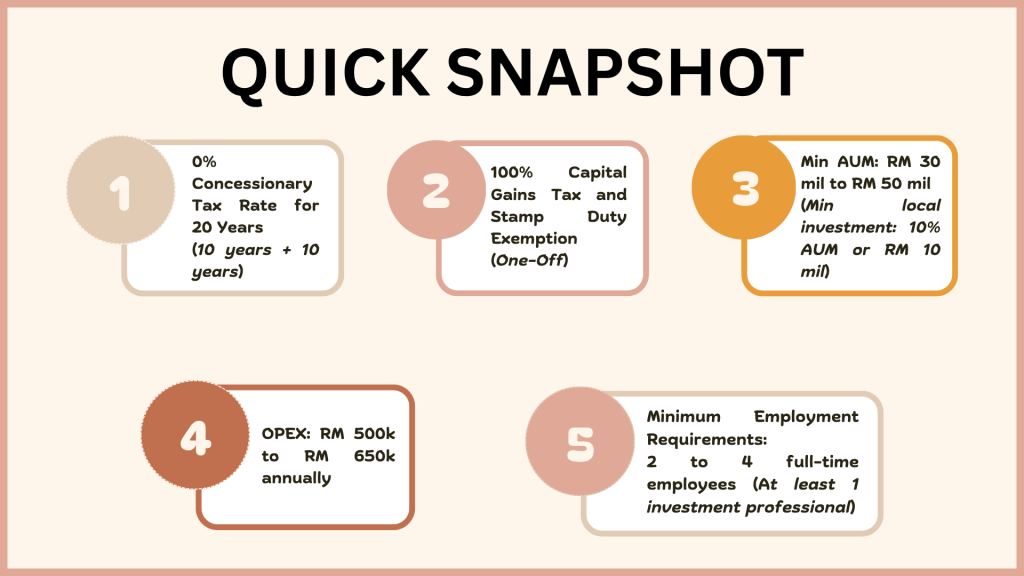

i. 0% concessionary tax rate for an initial period of 10 years, with a possible extension of another 10 years.

ii. 100% Capital Gains Tax (“CGT”) exemption upon initial establishment

iii. 100% stamp duty exemption upon initial establishment

|

Special individual income tax rate of 15% for knowledge workers and Malaysians working in Forest City SFZ. |

|

Form of Legal Entity |

i. Must be a newly incorporated investment holding company in Malaysia.

ii. Pre-registration with the SC is required to determine eligibility of the tax incentives. |

i. Must be a related company of the SFOV.

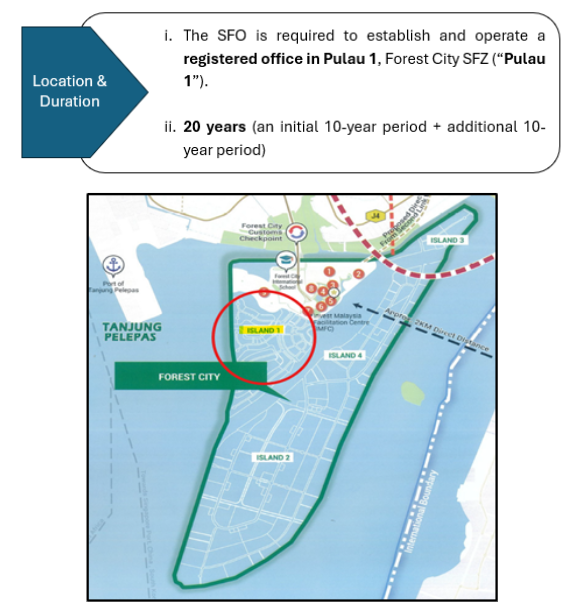

ii. Must be established and operating in Pulau 1. |

|

Licensing |

Two-step process for SFO Incentive Scheme Certification:

i. Consultation with the SC and stablishment of the SFO; & ii. Annual Tax Certification |

A fund management license under the Capital Markets and Services Act 2007 (“CMSA”) is required.

|

|

Employment Requirements |

Employ a minimum of 2 full-time employees (including 1 investment professional[4]), with a minimum monthly salary of RM10,000.00. | Employ a minimum of 1 investment professional with minimum monthly salary of RM10,000.00. |

|

Assets Under Management (“AUM”) |

i. Minimum AUM of RM30 million.

ii. Minimum local investment in eligible and promoted investments of at least 10% of AUM or RM10 million (whichever is lower). |

Management of SFOV’s assets:

1. Managing assets owned directly by the SFOV, or held by the SFOV as a beneficial owner through: i. A bank licensed by Bank Negara Malaysia (“BNM”); or ii. A capital market intermediary, whether the assets are maintained with a local or foreign custodian in Malaysia. 2. If management of the SFOV’s assets is delegated:

3. If management of the SFOV’s assets is NOT delegated:

|

|

Local Operating Expenditure[5] (“OPEX”) |

Incur at least RM500,000 annually. | N/A |

|

Criteria |

SFOV |

SFO MC |

|

Employment Requirements |

Employ a minimum of 4 full-time employees. | N/A |

|

Assets Under Management (“AUM”) |

i. Minimum AUM of RM50 million.

ii. Minimum local investment in eligible and promoted investments of at least 10% of AUM or RM10 million (whichever is higher). |

Same as Initial Period. |

|

Local Operating Expenditure (“OPEX”) |

Incur at least RM650,000 annually (30% higher than during the Initial Period). | N/A |

Two-Step Process for an SFO to Benefit from Tax Incentives under the SFO Scheme

To benefit from the SFO Incentive Scheme, prospective applicants must undergo a two-step process with the SC for the SFO Incentive Scheme Certification.

1. Step 1: Consultation with the SC and Establishing an SFO

a. Consultation with the SC

Prospective applicants must initiate a consultation with the SC by writing to SFOScheme@seccom.com.my.

b. Establishing the SFO Structure

Following the consultation, the applicant may proceed to establish the SFOV and the SFO MC.

c. Conditional Approval Letter

Once the SFOV is set up, the prospective applicants must submit all relevant documents to the SC. Upon complete documentation, the SC will issue a Conditional Approval Letter (“Conditional Approval Letter”). This is a pre-requisite for the subsequent annual tax certification.

d. One-Off Exemptions at Establishment

At the point of establishment, the SFOV may also apply for one-off exemptions from CGT and stamp duty on the transfer of qualifying assets into the SFOV.

This requires the submission of completed forms and supporting documents to the SC. If all conditions are met, the SC will issue a verification letter confirming eligibility for these one-time exemptions.

2. Step 2: Annual Tax Certification

The SFOV must apply for annual tax certification by submitting the following to the SC:

a. The SFOV Tax Certification Form.

b. Audited accounts.

c. Other supporting documents (if any).

If the SC is satisfied that the criteria are met, it will issue a Certification Letter. This letter enables the SFOV to claim tax exemption from the Inland Revenue Board of Malaysia (“IRBM”).

Other Key Benefits of the SFO Incentive Scheme

1. Foreign Exchange Flexibility

a. No limit on investments in foreign currency assets (if sourced from abroad or non-residents)

b. No restriction on offshore borrowings for overseas activities or operations within Forest City SFZ

c. BNM’s commitment to facilitating cross-border fund movements to ease inflows/outflows and promote Malaysia as a regional wealth management hub[6].

2. Resident Pass-Talent (“RPT”) Visa[7]

Supports the relocation of both foreign professionals working within the SFO structure and family members of the single wealthy family. This RPT visa is aligned with the duration of the SFO scheme, providing residency for up to 20 years (i.e., Initial Period and Additional Period).

The SC is working closely with the Ministry of Home Affairs via TalentCorp to facilitate this process.

Key Criteria Comparison: Malaysia, Singapore, and Hong Kong[8]

|

Criteria |

Malaysia | Singapore[9] |

Hong Kong[10] |

|

Tax Incentives |

i. 0% concessionary rate for 20 years (Initial Period and Additional Period); &

ii. One-off exemptions for capital gains tax and stamp duty |

i. Offshore Fund Exemption Scheme (13D);

ii. Onshore Fund Incentive Scheme (13O); & iii. Enhanced Tier Tax Incentive Scheme (13U). |

0% concessionary profits tax rate earned from qualifying and incidental transactions for eligible Family-owned Investment Holding Vehicles (FIHVs) and Family-owned Investment Holding Vehicles (FSPEs). |

|

Employment Requirements |

A minimum of 2 full-time employees (including 1 investment professional) | A minimum of 2 local qualified investment professionals (at least 1 must not be a family member) | A minimum of 2 full-time employees (can be family members) |

|

Minimum AUM |

RM30 million (Initial Period) to RM50 million (Additional Period) | SGD20 million | HKD240 million |

|

Minimum OPEX |

RM500,000 (Initial Period) and RM650,000 (Additional Period) | SGD200,000 | HKD2 million |

Note: The employment requirements, minimum AUM, and minimum OPEX in Singapore vary depending on the applicable tax incentive schemes under Sections 13D, 13O, and 13U of the Income Tax Act 1947.[11]

How does Malaysia compare? To start, Malaysia offers a lower entry threshold and operating expenditure compared to Singapore and Hong Kong, making it more accessible. In addition to a 0% tax rate for up to 20 years, one-off exemptions for CGT and stamp duty help reduce initial set-up costs.

How Can Lawyers Help? The Role of Legal Advisors in the SFO Setup Process

As highlighted in the keynote address delivered by Datin Paduka Azalina Adham, Managing Director of the SC, during the SFO Summit on 22.5.2025, “Service providers play a very important role and are critical components of the SFO scheme. Families would need to rely on an array of professional advisers from law firms to tax advisors to trustees, capital market players, fund managers, and bankers to support their growth here.”[12]

To that end, lawyers can play a key role in supporting the establishment of a Single Family Office (SFO) by:

Concluding Thoughts

Malaysia’s SFO Incentive Scheme signals a bold step toward positioning the country as a leading destination for family offices in Asia. With a 0% tax rate for up to 20 years, one-off exemptions for capital gains tax and stamp duty, and flexible foreign exchange policies, the scheme offers one of the most attractive packages in the region.

While regulatory clarity and implementation will be key to building investor confidence, Malaysia’s central location, mature Islamic finance ecosystem, and cost advantages offer strong foundational appeal.

As the framework continues to take shape, families considering the establishing of an SFO in Malaysia are encouraged to seek professional advice to ensure compliance and to fully leverage the available incentives.

For further information or assistance in setting up a SFO in Malaysia, please contact Partner Chris Toh Pei Roo (tpr@lh-ag.com), or Associates Jay Fong Jia Sheng (fjs@lh-ag.com) and Soon Jia Ying (jys@lh-ag.com).

REFERENCES

[1] See SC’s Frequently Asked Questions – Single Family Office Scheme (23 September 2024): https://www.sc.com.my/api/documentms/download.ashx?id=f327fb87-91eb-4947-8ef4-786226d2e3e6 See also: SC Family Office Incentive Scheme at https://www.sc.com.my/resources/media/media-release/sc-outlines-family-office-incentive-scheme

[2] See also: Keynote Address at Forest City Special Financial Zone Tax Incentive Announcement Ceremony (20 September 2024) at https://www.sc.com.my/resources/speeches/keynote-address-at-forest-city-special-financial-zone-tax-incentive-announcement-ceremony

[3] See SC Family Office Incentive Scheme at https://www.sc.com.my/resources/media/media-release/sc-outlines-family-office-incentive-scheme

[4] The investment professional must have at least 2 years of relevant working experience, and hold at a minimum, a degree recognised by the Malaysian Qualifications Agency (MQA), or possess a globally recognised finance-related professional certification including but not limited to a Master’s of Business Administration (MBA), Chartered Financial Analyst (CFA), Chartered Accountant, Chartered Banker, Certified Financial Planner or equivalent certifications.

[5] Local operating expenditure may include but not limited to employee remuneration (wages, salaries, bonuses), professional services, rental and utilises and management fees paid to the SFO MC.

[6] Keynote Address at Forest City Special Financial Zone Tax Incentive Announcement Ceremony (20 September 2024): https://www.sc.com.my/resources/speeches/keynote-address-at-forest-city-special-financial-zone-tax-incentive-announcement-ceremony

[7] Ibid.

[8] https://assets.kpmg.com/content/dam/kpmg/my/pdf/26-may-2025-nanyang-siang-pau-tai-lai-kok-elliot-chaw-family-offices-in-asia.pdf

[9] https://www.mas.gov.sg/schemes-and-initiatives/fund-tax-incentive-scheme-for-family-offices

[10] https://www.ird.gov.hk/eng/tax/bus_fihv.htm

[11] https://www.aseanbriefing.com/news/tax-incentive-requirements-for-family-offices-in-singapore/

[12] https://www.sc.com.my/resources/speeches/keynote-address-at-single-family-office-summit